Question: What sort of tax break will the the Tiverton Glen development get?

Tiverton residents who oppose the mixed-use development proposed for the undeveloped land between Souza Rd. and Route 24 (between Main Rd. and Fish Rd.) have plenty of bad things to say about the idea. One issue that has been less fully explored than traffic and comprehensive plan changes and historic districts, however, might persuade even tax-hawks who generally favor development: tax deals.

If there are any such give-mes directly included in the proposal, they aren’t obvious. There isn’t an explicit request for tax subsidies, and the documents available on the town Planning Board’s page don’t say anything about the tax breaks that often come with affordable housing in large developments. Indeed, the three fiscal impact statements all assume that tax rates will be standard. Whether that is accurate or is an oversight is beyond the scope of this post to determine.

However, Tiverton also has an economic development tax break that would probably apply. Town Ordinance Chapter 74, Division 5, lays out a tax phase-in available to commercial and industrial construction and renovation within an enterprise zone (which appears to include the entire town). Some of the structures in the Tiverton Glen plan include both commercial and residential property, and it isn’t clear whether the ordinance would assign each building to one use or divide it into portions for tax purposes. In this post, I’ll assume all buildings get the full deal, so the numbers represent a maximum.

Basically, once the property is in use, the real property taxes are waived for one year and then phased in by 20% by year, so by the sixth year, the owner pays full taxes on the real estate.

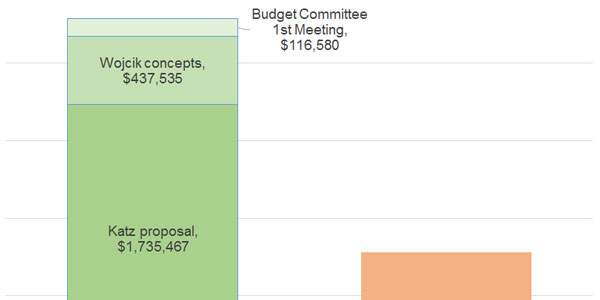

Both the developer and an independent organization hired by the town have analyzed the fiscal impact of the development. The developer concluded that there would be about $3.0 million in new revenue for the town and $1.3 million in costs to the town. The independent contractor put the numbers at $2.1 million and $0.2 million, so the developer’s estimate was actually more pessimistic.

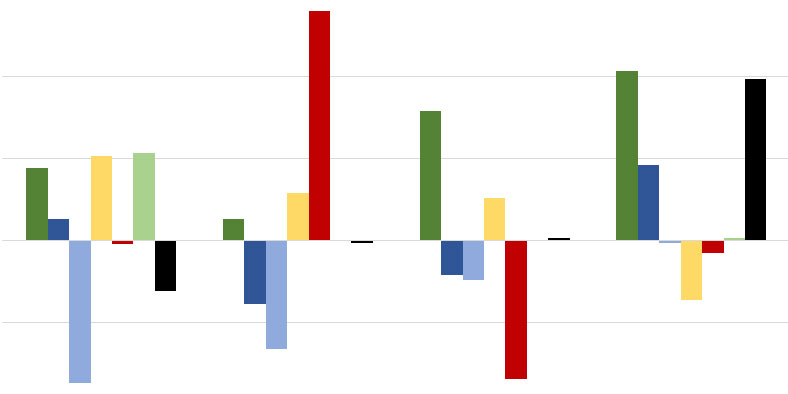

Applying the ordinance’s phase-in to just the property tax portion of the estimates, the developer’s estimates would provide a $1.2 million tax break in the first year after completion, dropping to $659,976 in year two and $74,876 in year, turning positive the following year. The independent analysis would put the first-year loss for the town at $64,000, turning positive the next year. Averaging the two would produce a $654,538 loss in the first year, and a $162,288 loss in the second year, and positive increases thereafter.

A “loss” means that other taxpayers would wind up covering this much in town costs for the development. Of course, that assumes that the development is fully operational (for both revenue and costs) in year one. If the developer puts up the residential portions first and families with children are the first to move in, that would produce much bigger costs in the earlier years. In contrast, if the hotel and restaurant structures go up first (producing the additional hospitality taxes that the state will forward to the town), then the early years would look much better.

Whether these dollar amounts ought to scare residents off of the project is up for them to decide. Whatever the case, it should be a subject of discussion, and well understood before final approval is given, because the town potentially faces a significant bill some year in the near future.