-

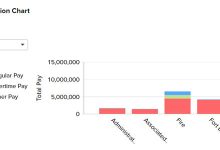

The town has already collected $4 million of a possible $13 million in extra money hidden from the budget process.

News & Commentary

-

Original Reports

Council’s Illegal Off-Budget Spending Needs to Be Corrected, Not Expanded

One point of contention in the political wrangling over Tiverton's future gambling revenue is whether the Town Council can set up restricted accounts outside of the town's ordinary budget process (including the financial town referendum [FTR]) and put dedicated revenue into them. Town Solicitor Anthony DeSisto seems to have advised the council that it can do so. That advice is incorrect. Tiverton's Home Rule Charter is unambiguous that all anticipated revenue of the town must be accounted for in the budgeting process. In Section 503(1), dealing with the town administrator's "duties and powers" in the budgeting process, the charter states: The Municipal budget, as proposed by the Town Administrator shall include all anticipated revenues and expenditures, except those for the school purposes, and the total of such expenditures shall not be greater than the total of the anticipated revenue. He/She shall incorporate the total of these expenditures and revenues with the total he/she has arrived at for general town purposes. According to the town's budgeting process described in Section 301, the administrator's budget is the starting point for the municipal budget, period. Restricted funds can be noted as such, so the council and Budget Committee know that they cannot be changed, but they must be part of the discussion. Just as clearly, the council has no authority to create those restricted funds outside the regular budget process without a direct vote of the people. Section 1214 of the charter states: All fees, penalties, payments and miscellaneous sources of revenue including…

Read More » -

-

-

Resources

-

Resources

Documents

Links to documents relevant to town government that may or may not be available elsewhere.

Read More » -